Trump’s WLFI Had Already Lost Half Its Value Then Private Sales and a New Supply Overhang Came to Light.

By April 2026, Trump's WLFI had already lost roughly half its value for the year. The price decline was visible. What investors could not see was who controlled billions of locked tokens—and how much of that supply might eventually gain a path toward liquidity.

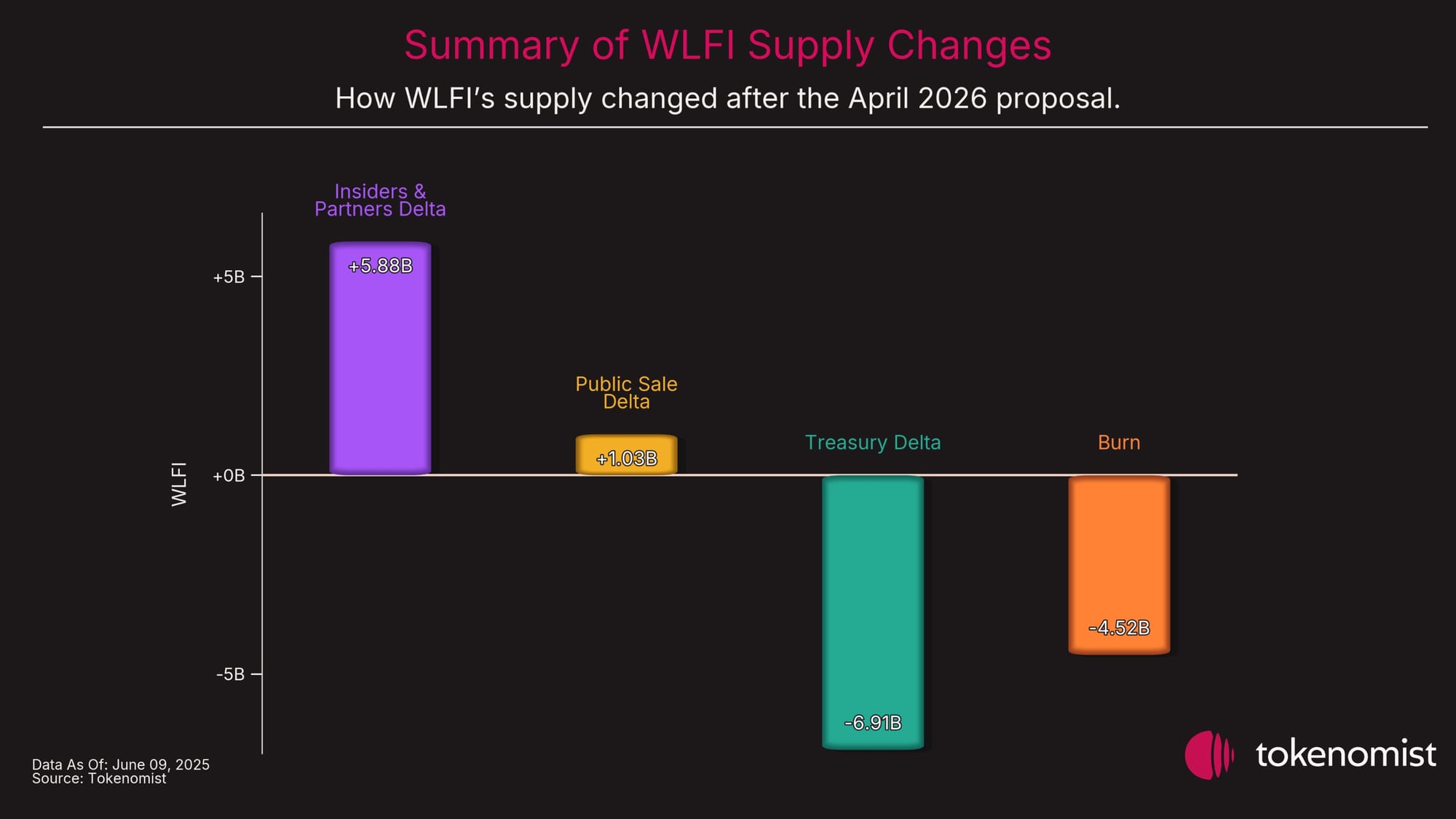

Key Takeaways

- WLFI had lost about half its value in 2026 when news of private token sales emerged. While the timing does not prove causation, it introduces additional risk for investors evaluating the token’s outlook.

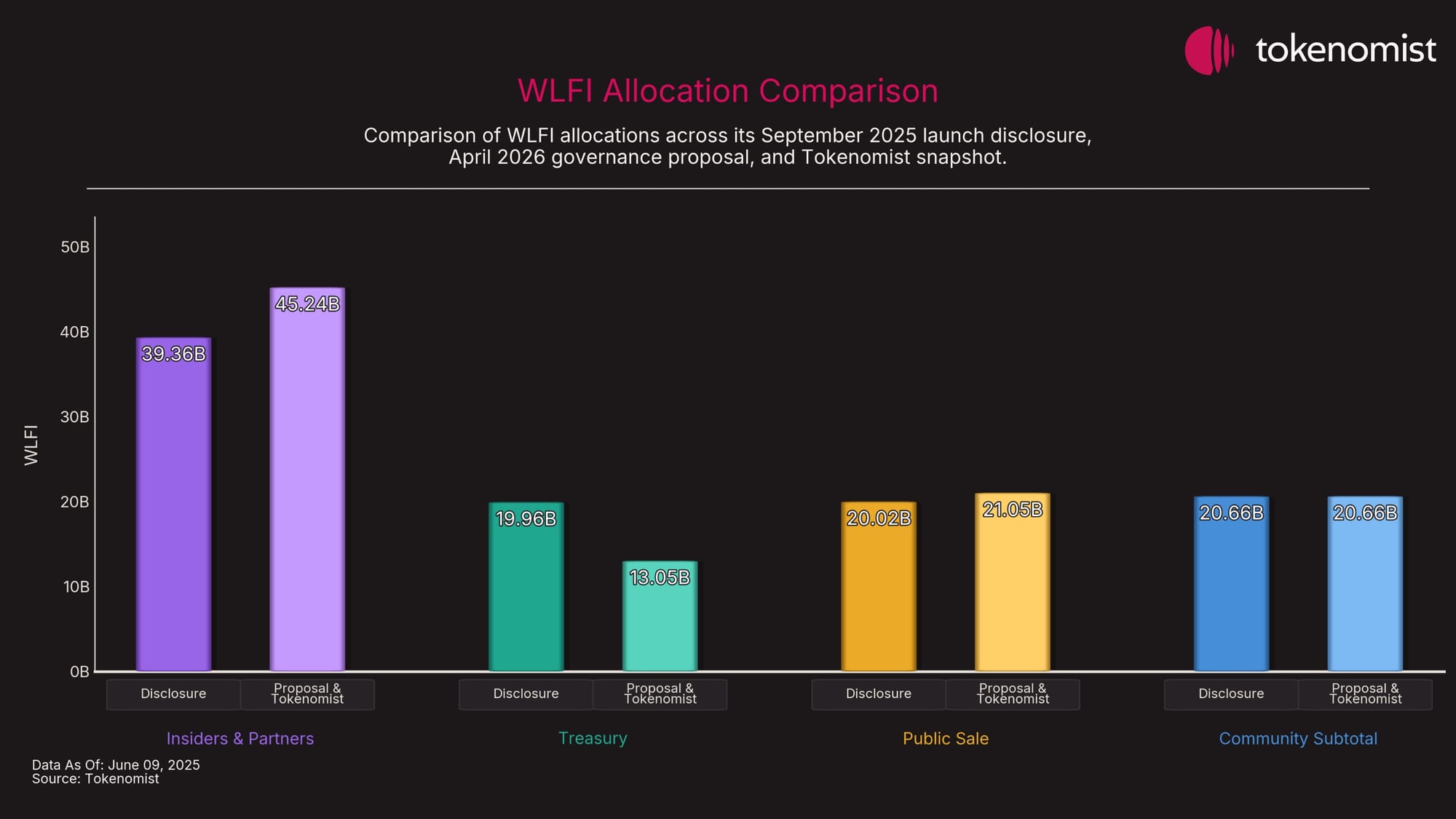

- WLFI’s April 2026 proposal listed 45.24B tokens for founders, team members, advisers, and partners, which is 5.88B more than originally disclosed. WLFI later attributed this difference to private Treasury sales, Bloomberg reported.

- The private sales did not increase WLFI’s 100B maximum supply, but they changed who controls part of it. Treasury-controlled tokens became privately held supply with undisclosed buyers, prices, and complete lockup terms.

- The maximum 4.52B token burn reduces, but does not eliminate, the supply overhang. With full participation, up to 40.71B WLFI could enter a two-year cliff, then three years of linear vesting.

- WLFI’s future price will significantly depend on the actions of private holders once their tokens unlock. Investors should monitor actual burn transactions, holder participation, and vesting activity, rather than assuming maximum figures have been executed.

What Is WLFI?

WLFI is the governance token of World Liberty Financial, a DeFi project launched in 2024 and backed by Donald Trump and his family.WLFI is a governance token, not equity. Eligible holders may vote on governance proposals, subject to protocol rules and limits. Proposals may address protocol development, ecosystem initiatives, treasury use, and token unlock schedules.

However, holding WLFI does not confer equity ownership, dividend rights, revenue sharing, or any direct claim on World Liberty Financial’s income or assets. The project’s Gold Paper explicitly separates WLFI governance rights from financial ownership. The project operates two primary products:

· WLFI — the protocol's governance token.

· USD1 — a US dollar-pegged stablecoin backed by eligible reserve assets, including short-term US government securities, bank deposits, and cash equivalents. BitGo provides custody and reserve infrastructure.

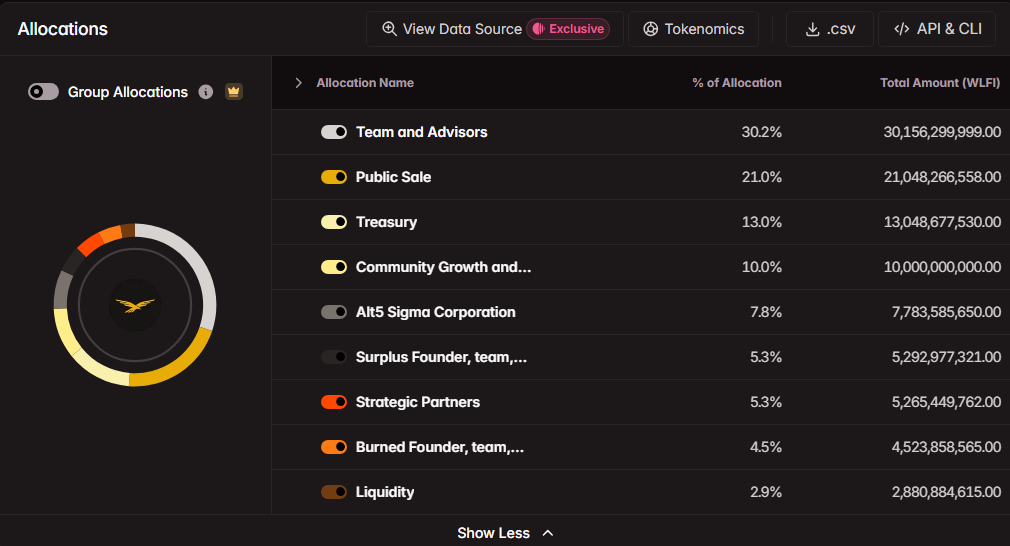

The official WLFI tokenomics documentation states WLFI launched with a maximum supply of 100 billion tokens, allocated across four main categories:

- Token Sale = 33.893%

= 33,893,000,000 - Community Growth and Incentives = 32.6%

= 32,600,000,000 - Co-Founder Allocation = 30%

= 30,000,000,000 - Team and Advisors = 3.507%

= 3,507,000,000

WLFI’s April Proposal Listed 45.24B Tokens, 5.88B More Than Its Earlier Disclosure

The earlier disclosure placed 39.36B WLFI across Team, Advisors, and Strategic Partners. The April proposal later grouped founders, team members, advisors, and partners into a 45.24B WLFI locked allocation.

The proposal did not reconcile the increase. WLFI later confirmed private Treasury sales had occurred, but did not disclose the number of tokens sold or the transaction terms.

Allocation Comparison: Before and After

Explore the full WLFI allocation table in [Google Sheets].

Reconstructing the Gap

In the September 2025 disclosure, the comparable allocations were:

- Team & Advisors: 33,506,999,999 WLFI

- Strategic Partners: 5,850,499,736 WLFI

- Combined: 39,357,499,735 WLFI

The April 15, 2026, governance proposal was subsequently identified:

- Founder, team, advisor, and partner locked tokens: 45,238,585,647 WLFI

The difference is:

45,238,585,647

− 39,357,499,735

─────────────────

= 5,881,085,912 WLFI

The two disclosures do not use identical category labels, so the comparison should not be interpreted as a perfect accounting reconciliation. However, they describe substantially comparable insider-and-partner supply pools. The April proposal did not explain why the reported allocation had increased, nor did it reconcile the 45.24B figure with the September disclosure.

The April 2026 governance proposal did not explain this increase. It did not reference the September 2025 disclosure. It simply listed 45.24B as the current insider/partner locked total and used that figure as the basis for the proposed vesting schedule.

After Tokenomist identified the 5.88B allocation gap, Bloomberg asked World Liberty Financial for clarification. The project confirmed that private “white glove” Treasury sales to accredited investors had occurred, but it did not publicly specify the number of tokens sold, according to Bloomberg’s May 1, 2026 report.

WLFI’s Explanation

After Bloomberg sought clarification, World Liberty Financial confirmed that private “white glove” treasury sales to accredited investors had occurred. However, the project did not publicly specify the number of tokens sold or disclose the buyers, sale prices, lockup terms, or transfer restrictions. The 5.88B WLFI figure is Tokenomist’s calculation based on the increase in the comparable FTA&P allocation, not a quantity stated by World Liberty Financial.

The Treasury allocation declined by about 6.91B WLFI, exceeding the 5.88B FTA&P increase by roughly 1.03B. This difference aligns with the increase in Public Sale/Early Supporters and a 400,000-WLFI adjustment in Community/Other. These figures reconcile the totals but do not provide on-chain proof of specific transfers.

What the Delta Does—and Does Not—Show

The 5.88B delta is not evidence that new tokens were minted. WLFI’s maximum supply remained 100B. Nor does the document comparison alone provide on-chain proof of the reported private sales.

This establishes a disclosure gap: the founder, team, advisor, and partner allocation increased by about 5.88B WLFI between the September 2025 and April 2026 disclosures, without reconciliation in the proposal. WLFI later attributed the increase to the private Treasury sales. However, due to differing category labels and a lack of wallet-level data, this comparison cannot independently confirm how tokens moved between allocations.

Scope note: “100B” refers to WLFI’s maximum supply ceiling; these allocation changes did not create new tokens. A separate Reuters analysis identified an approximately 3B decline in issuer-retained WLFI between September and October 2025. The October disclosure reported 29,853,140,794 WLFI as issuer-retained assets in WLF’s MiCA white paper, section G.5. Reuters concluded that the tokens were probably sold. Because WLF did not confirm the sale, and available records cannot establish whether it overlaps with the 5.88B gap, the 3B figure is excluded from this analysis.

WLFI’s Future Price Risk Changed When Treasury Tokens Moved to Private Buyers

Tokenomist’s snapshot as of May 12, 2026, shows WLFI’s Treasury allocation at 13,048,677,530 tokens, down about 6.91B from 19,955,030,000 in September 2025. Selling Treasury tokens does not mint new tokens or increase the 100B maximum supply; it changes who controls part of the existing supply economically.

Before the private sale

Treasury reserve → controlled by the project and available for future protocol use.

Supply risk → depends primarily on the project’s deployment decisions.

After the private sale

Investor-owned allocation → controlled by private holders, subject to any applicable lockup, vesting, or transfer restrictions.

Supply risk → increasingly depends on investor incentives and eventual exit decisions.

The tokens were always part of the total supply, so the sale does not create literal dilution. However, it converts project-controlled reserves into investor-owned supply, making future liquidity more likely. This can affect market perceptions of ownership concentration, future float, and potential selling pressure.

Why ownership matters for supply state: Private sales changed the nature of supply risk. Protocol-controlled reserves depend on project deployment decisions, while privately held allocations depend on holder incentives once restrictions expire. Since transaction terms are undisclosed, the timing and scale of potential market entry remain uncertain.

The April 2026 Proposal Made WLFI’s Future Selling Pressure Easier to See

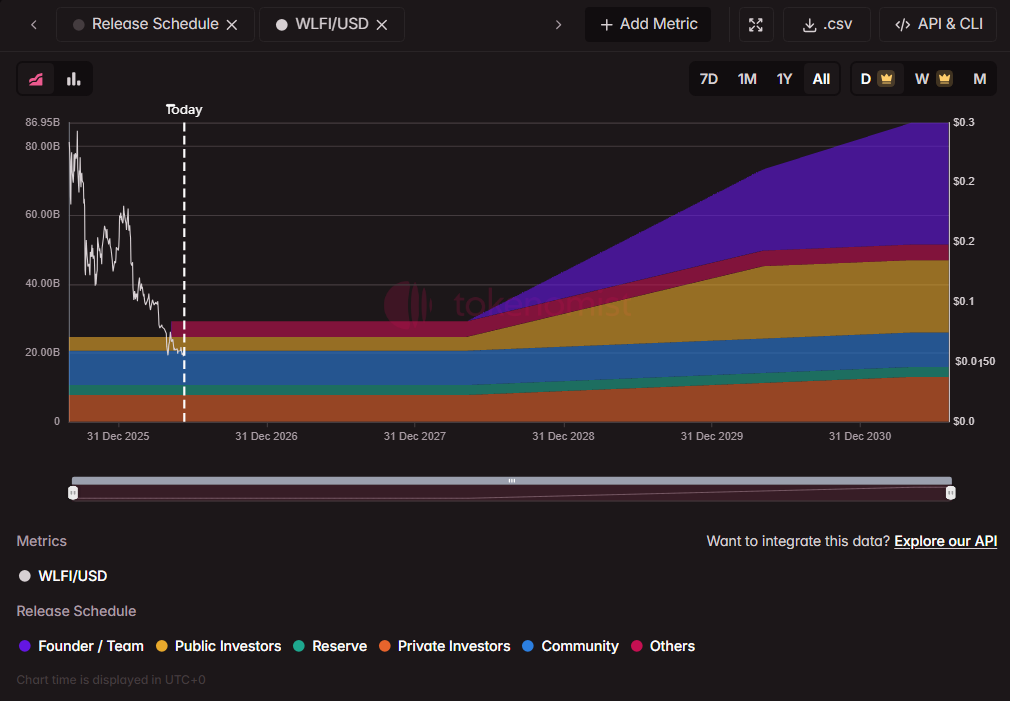

The April 15, 2026, governance proposal gave eligible holders a choice: accept a defined vesting schedule or keep their tokens locked indefinitely.

Early Supporters: No Burn Required

The proposal covered 17,043,666,558 WLFI held by Early Supporters:

· 2-year cliff unlock from proposal passage date

· 2-year linear vest after the cliff

· Full distribution: approximately year 4 from passage

· No tokens burned

FTA&P Holders: A 10% Burn to Enter Vesting

The proposal also covered 45,238,585,647 WLFI allocated to founders, team members, advisors, and partners. Participating holders must permanently burn 10% of the allocation they enroll before the remaining tokens can enter the vesting schedule. If the entire eligible pool participates:

· Maximum burn: 4,523,858,565 WLFI

· Maximum post-burn allocation: 40,714,727,082 WLFI

· Vesting schedule: Two-year cliff unlock followed by three years of linear vesting

· Full distribution: Approximately five years after the schedule begins

The burn applied only to holders who chose to participate; it was not automatic for the entire allocation. Non-participating holders kept governance rights, and their tokens remained locked indefinitely.

The proposal passed at Snapshot block 24,987,225, with 11,195,682,402.51 WLFI voting YES and 11,151,317.11 WLFI voting NO, equivalent to approximately 99.90% support among votes cast. This analysis does not attribute voting wallets to specific holder categories.

Fewer Tokens, More Supply Pressure: What Happens Next for WLFI?

WLFI’s supply is moving in two opposing directions.

WLFI’s allocation shifted in two stages. The Insiders & Partners pool increased by 5.88B WLFI, while Public Sale increased by 1.03B, and Treasury declined by 6.91B. WLFI later attributed the 5.88B increase to private Treasury sales. Separately, the April 2026 proposal introduced a maximum conditional burn of 4.52B WLFI and a vesting path for up to 40.71B WLFI under full holder participation.

The proposed burn reduces the number of tokens that could reach the market. If fully executed, up to 4.52B WLFI would be permanently removed from supply. The new vesting schedule would give the remaining 40.71B founder, team, advisor, and partner tokens a defined path from indefinite lock to future liquidity.

This could reduce the maximum token count and make the timing of future unlocked supply more transparent. It does not create an immediate circulating supply or guarantee future selling pressure.

Treasury Reallocation Changed Who Controls the Supply

The Treasury declined by about 6.91B WLFI between the September 2025 disclosure and Tokenomist’s snapshot. During the same period, the FTA&P pool increased by about 5.88B WLFI, the Public Sale/Early Supporter allocation by about 1.03B WLFI, and a 400,000-WLFI adjustment appeared in Community/Other. These changes reconcile the 100B maximum supply at the allocation level.

WLFI attributed the 5.9B increase in FTA&P to private Treasury sales. The separate 1.03B Early Supporter increase may reflect additional eligible claimants, as described in the governance proposal. These changes do not provide wallet-level proof that the entire 6.91B Treasury reduction was sold to private investors.

The Burn Reduces the Size of the Future Unlock

The burn is part of the mechanism that converts an indefinitely locked allocation into a defined vesting schedule. It should not be viewed as a separate offset to the entire FTA&P allocation.

FTA&P holders who opt in must permanently burn 10% of their locked allocation. The remaining 90% enters a two-year cliff, then three years of linear vesting. With full participation, up to 4.52B WLFI would be burned, and up to 40.71B WLFI would enter the vesting schedule.

These changes have two effects: fewer tokens are eligible for future release, and the post-burn allocation gains a defined path to potential liquidity. The maximum scheduled amount is 40.71B WLFI, but the actual amount depends on holder participation. Scheduled or unlocked tokens are not immediately circulating or sold.

WLFI Warning Signs Investors Should Not Ignore

Disclosure risk. Token allocation figures can change between the original launch disclosure and later governance records without clear reconciliation. Identifying discrepancies requires tracking allocations across multiple documents over time; these changes do not appear automatically in price data or standard market metrics.

Treasury discretion risk. OTC and private treasury sales are common in the industry. Privately sold treasury tokens shift from protocol-controlled reserves to investor-owned supply. Supply models treating all treasury tokens as non-circulating may understate future float risk if many have been privately placed, though the timing and likelihood of sales remain unknown.

Governance controls risk. Locked WLFI retains voting rights, so the circulating supply does not fully reflect the distribution of governance power. Although the proposal passed with about 99.90% support, wallet-level attribution is needed to determine which groups of holders supported it.

Unlock risk. Indefinite locks are not permanent. As shown in April 2026, a governance vote can convert an indefinitely locked pool into a defined vesting schedule. Indefinite locks should be treated as conditional deferrals, not as permanent removals from future supply.

Valuation risk. Token sale proceeds, treasury-controlled allocations, privately placed tokens, and governance-locked tokens should be modeled as separate supply categories with distinct behavioral assumptions. FDV accounts for full supply but does not distinguish between protocol reserves, private investor holdings, and team allocations, each with different incentives and liquidity timelines.

Holder transparency risk. The identities, entry prices, lockup terms, and investment horizons of private buyers have not been disclosed. Without this information, the market cannot reliably assess ownership concentration, holder incentives, or the likelihood and timing of future liquidity events.

Implementation risk. The proposal defines the broad vesting framework, but some implementation details remain subject to confirmation, such as the extent of holder participation and the on-chain burn execution status. Actual future supply will depend on which holders opt in, how much is burned, and how unlock contracts are implemented.

This analysis distinguishes three evidence layers: public records, calculated comparisons, and reported project responses. Official disclosures and governance records establish the figures. The 5.88B WLFI gap is a document-level calculation, while the private-sale explanation comes from World Liberty Financial’s response as reported by Bloomberg.

Source

Official WLFI Documents

- World Liberty Financial. “WLFI Tokenomics.” Accessed June 11, 2026.

- World Liberty Financial. “WLFI Unlock Documentation.” Accessed June 11, 2026.

- World Liberty Financial. “WLFI Risk Disclosures.” Accessed June 11, 2026.

- World Liberty Financial. "Understanding the WLFI Circulating Supply at Launch." Medium, September 1, 2025.

- World Liberty Financial. “MiCAR White Paper.” Version 1.1, Section G.5, “Issuer Retained Crypto-Assets.” Notified October 30, 2025.

Governance and On-Chain Records

- World Liberty Financial Governance. “Early Supporter & Founder/Team/Partner Token Unlock Proposal.” April 15, 2026

- Snapshot. “Early Supporter & Founder/Team/Partner Token Unlock Vote.” Voting closed May 6, 2026; snapshot block 24,987,225.

- Ethereum. "World Liberty Financial Unlock Contract."

0x74B4f6A2E579D730aAcb9dD23cfbbAEb95029583. Cliff timestamp:1841245200(May 6, 2028 17:00 UTC); end timestamp:1935853200(May 6, 2031 17:00 UTC). Verified on Etherscan.).

Tokenomist Data

- Tokenomist. “World Liberty Financial (WLFI) Allocation Tracker.” Data last updated May 12, 2026; accessed June 5, 2026.

- Tokenomist. “WLFI Unlock Events.” Accessed June 5, 2026.

Bloomberg Reporting

- Bloomberg. “Trump Family Crypto Project Quietly Sold as Holders Got Stuck.” May 1, 2026.

- Bloomberg. “Quiet Token Sales Boosted Trump Crypto Wealth by $660 Million.” May 12, 2026.

Reuters Reporting

- Reuters. “Under the Trump Crypto Playbook, the Family Always Wins. Investors Don’t.” June 9, 2026.

Reproduce This Analysis With the Tokenomist API

The Tokenomist data used in this analysis can also be retrieved programmatically through the tok CLI:

- Tokenomist API. WLFI allocation data retrieved with

tok allocation detail world-liberty-financial --output json. Data last updated May 12, 2026; accessed June 5, 2026. View WLFI on Tokenomist. - Tokenomist API. WLFI unlock data retrieved with

tok unlock events world-liberty-financial --output json. Accessed June 5, 2026. View WLFI unlock events.

Build with Tokenomist API

Access standardized token allocation, unlock, fundraising, emission, burn, and buyback data. Empower your AI agents with reliable tokenomics data, automate supply monitoring, build internal dashboards, and integrate supply-side intelligence into your research workflow.

Explore Tokenomist API →

FAQ

Q: What exactly is the 5.88B gap?

It is the difference between the comparable insider/partner allocation in WLFI’s September 2025 launch record (39.36B WLFI) and the April 2026 governance proposal (45.24B WLFI). The 5.88B gap reflects a change in the classification of existing supply, not newly minted tokens.

Q: Did WLFI do anything illegal?

This article does not reach a legal conclusion. WLFI told Bloomberg that the tokens were sold to accredited private investors, but the public tokenomics records alone cannot establish whether the sales complied with all applicable laws.

Q: How did Tokenomist find this?

Tokenomist compared WLFI’s September 2025 allocation record with its April 2026 governance proposal. The 5.88B difference was not clearly reconciled in the proposal.

Q: What does "white glove" mean?

“White glove” was WLFI’s reported description of the private transactions. It is not a standardized legal term. Bloomberg reported that the buyers were accredited private investors, but their identities, prices, and complete terms were not disclosed.

Q: When does the cliff unlock occur?

"The unlock contract sets a hard cliff of May 6, 2028, at 17:00 UTC (Unix timestamp1841245200, on-chain at 0x74B4f6A2E579D730aAcb9dD23cfbbAEb95029583), with linear vesting running through May 6, 2031, at 17:00 UTC. This is a fixed date written into the contract — not an estimate. The full allocation does not unlock at once."

Q: Do WLFI holders receive a share of token-sale proceeds?

No. WLFI provides governance rights but does not grant holders equity, dividends, or revenue-sharing rights. World Liberty Financial’s disclosures state that DT Marks DEFI LLC is entitled to 75% of WLFI token-sale proceeds after agreed deductions. This arrangement does not entitle WLFI holders to a share of those proceeds. (World Liberty Financial - WLFI Risk Disclosures, 2025)

Source: World Liberty Financial Gold Paper and Risk Disclosures, accessed June 5, 2026.

Q: Why does the 10% burn matter for the analysis?

The burn is the cost of entering the new vesting schedule. Founders, team members, advisors, and partners who participate must permanently burn 10% of their locked allocation. If all eligible holders opt in, up to 4,523,858,565 WLFI would be removed from the total supply and would not be recoverable through future governance actions. In exchange, the remaining 90% receives a defined path toward future liquidity: a two-year cliff followed by three years of linear vesting. The burn therefore reduces the overall supply overhang, while converting the remaining allocation from an indefinite lock into scheduled future supply.

Q: Is USD1 affected by the WLFI allocation discrepancy?

Not directly. The discrepancy concerns the allocation and ownership of the WLFI governance token. USD1 is separately issued and redeemed by BitGo and backed by its own reserve assets. Nothing in the WLFI allocation discrepancy, by itself, indicates a shortfall in USD1 reserves.